BIS moves tokenization into live payments

The BIS will move Project Agorá from prototype tests to live cross-border payments using real money.

The BIS will move Project Agorá from prototype tests to live cross-border payments using real money.

The Bank for International Settlements is taking its tokenization work out of the lab and into live payment tests. Project Agorá has already linked seven central banks and more than 40 financial institutions, and the next phase will use real-value transactions instead of synthetic ones.

| Metric | Value | Why it matters |

|---|---|---|

| Participating central banks | 7 | Shows the project has broad public-sector backing |

| Financial institutions involved | 40+ | Gives the trial enough private-sector weight to test real payment flows |

| Prototype status | Atomic settlement phase completed | The next step is live money, not simulation |

| Report length | 97 pages | Signals the BIS is treating this as a full systems review |

| Next checkpoint | Mid-2026 update | That is the first real test of whether the model works at scale |

What Project Agorá actually tested

Get the latest AI news in your inbox

Weekly picks of model releases, tools, and deep dives — no spam, unsubscribe anytime.

No spam. Unsubscribe at any time.

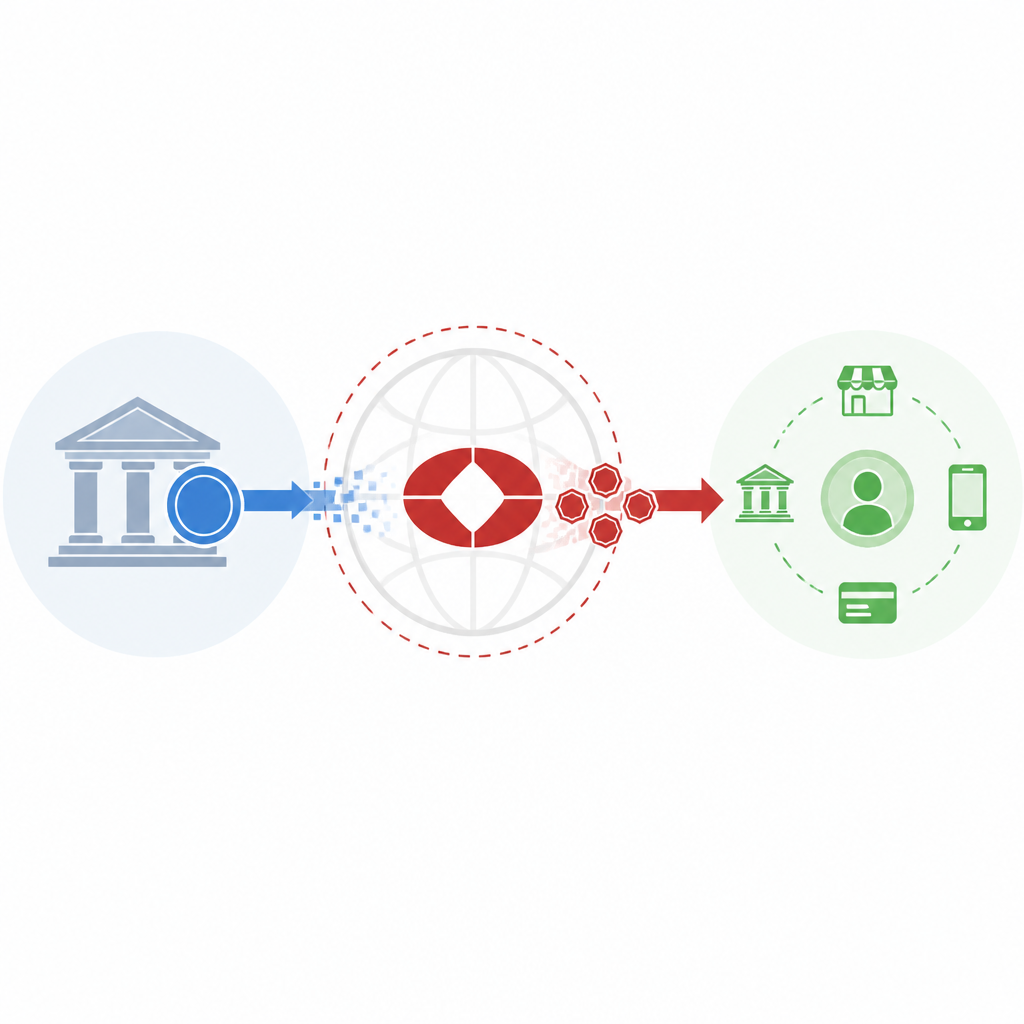

Project Agorá is the BIS Innovation Hub’s answer to a very old problem: cross-border payments are slow, expensive, and full of manual handoffs. The prototype showed that tokenised commercial bank deposits can settle against tokenised central bank reserves on a shared platform, with finality across jurisdictions.

The technical idea is simple enough to explain without the jargon. If every leg of a transaction is ready, the system settles everything at once. If one part fails, nothing moves. That is atomic settlement, and it is the opposite of the messy partial execution that can create reconciliation headaches in correspondent banking.

According to the BIS announcement, the prototype compresses flows that can take days into seconds. That is a big claim, but it is also the kind of claim central banks can only make after proving the system can handle compliance, finality, and legal differences across borders.

- Settlement happens in one step instead of many partial steps.

- Compliance checks stay inside the payment flow.

- The system is designed to work with existing bank rails, including SWIFT and ISO 20022.

- The model keeps correspondent banking in place instead of trying to replace it.

Why the BIS is not trying to wipe out banks

This is where Project Agorá gets interesting. A lot of crypto payment projects pitch themselves as replacements for the banking stack. The BIS took the opposite route. Its 97-page report calls correspondent banking the “backbone of global payments” and keeps sanctions screening and anti-money-laundering controls inside the system.

That choice matters because it tells you what the BIS thinks tokenization is for. The goal is not to create a parallel financial system. The goal is to make the one that already exists move faster, with fewer manual steps and less operational risk.

“Once you know you have everything to run the transaction, you settle it in one go,” Andrea Maechler, Deputy General Manager of the BIS, said in remarks accompanying the release.

The quote gets to the heart of the design. The BIS is trying to reduce the friction that makes cross-border payments slow, while keeping the controls regulators care about. That is a very different bet from the one made by stablecoin networks, which usually focus on replacing correspondent layers with on-chain settlement.

There is also a practical reason for this approach. Banks already know how to screen payments, handle jurisdiction-specific rules, and manage settlement risk. If tokenization can slot into those workflows instead of forcing a full rewrite, adoption becomes much more plausible.

The participants tell you this is a serious test

The roster behind Project Agorá is not decorative. Alongside the BIS, the project includes the Bank of Canada, Bank of England, Federal Reserve Bank of New York, Bank of Japan, Banque de France, Swiss National Bank, Bank of Mexico, and Bank of Korea. The Institute of International Finance is coordinating the private-sector side.

That mix matters because cross-border payments fail in the seams between institutions, not inside a single controlled environment. If the BIS wants to prove that tokenized settlement can work across legal systems, it needs central banks, commercial banks, and market infrastructure firms all in the same room.

Bank of Canada Senior Deputy Governor Carolyn Rogers said tokenisation “has the potential to make these payments faster, cheaper and more efficient and secure,” confirming that the next phase will test actual money movement rather than just technical plumbing.

- BIS is moving from prototype to live-value trials.

- BIS Innovation Hub is running the project.

- Institute of International Finance is coordinating the private-sector side.

- Bank of Canada joined the project on Wednesday.

How this compares with the tokenization push on Wall Street

Project Agorá is part of a broader shift, but it is not the same thing as the tokenization efforts now spreading through market infrastructure firms. DTCC plans tokenized settlement for stocks, ETFs, and Treasuries. Nasdaq and ICE are building blockchain-based systems for tokenized equities.

Bernstein analysts have called 2026 a “tokenization supercycle,” pointing to rising stablecoin supply and on-chain Treasury demand. That framing is useful, but the BIS effort is more conservative and more institutional. It is trying to preserve the compliance and legal structure of banking while making settlement faster.

Here is the cleanest way to think about the difference:

- Wall Street tokenization is chasing market efficiency and new asset plumbing.

- BIS tokenization is chasing cross-border payment speed without breaking bank controls.

- Stablecoin rails aim to reduce dependence on correspondent banking.

- Project Agorá keeps correspondent banking and upgrades the rails underneath it.

The legal analysis in the BIS report also matters. It says settlement finality is achievable across all seven participating jurisdictions, but it adds that each legal regime still needs technical and contractual work. That is the kind of detail that separates a demo from a deployable system.

What to watch next

The next phase is the real test. Once actual money moves through the prototype, the BIS will learn whether tokenized settlement holds up under live operational pressure, not just clean pilot conditions. The final report is expected in the first half of this year, and the mid-2026 update will show whether the system can handle scale, compliance, and cross-border coordination at the same time.

If the trial works, central banks will have a template for faster international payments that still fits inside existing regulatory structures. If it breaks, the lesson will be just as useful: tokenization may solve some payment problems, but the hardest part is still the legal and operational glue between institutions.

My bet is that the mid-2026 update will matter more than the initial launch. That is the point where the industry will find out whether tokenized settlement is ready for real money, or still best kept inside carefully controlled pilots.

// Related Articles

- [IND]

OpenAI’s IPO filing turns hype into scrutiny

- [IND]

Skatteetaten proves public sector AI should be judged by outcomes

- [IND]

OpenAI’s IPO filing puts AI’s biggest test on Wall Street

- [IND]

OpenAI’s latest moves now center on pricing, safety, and scale

- [IND]

RISC-V mini PCs are worth buying now, but only as a bet on the future

- [IND]

Fedora 44 RISC-V widens Linux board support