Allianz: Hail Is Driving Bigger Storm Losses

Allianz says severe convective storms caused $60B in insured losses last year, with hail driving 50% to 80% of the damage.

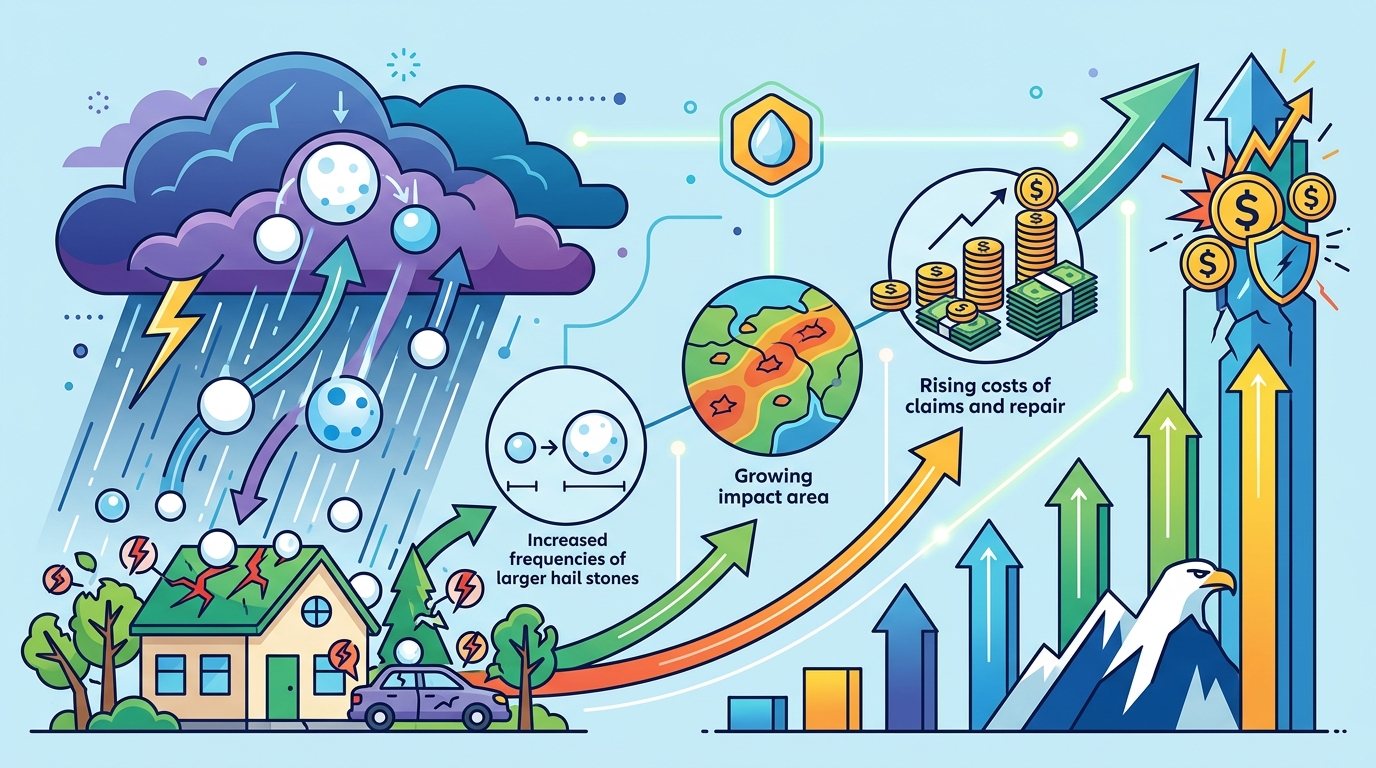

Severe convective storms caused about $60 billion in insured losses last year, and Allianz says hail is doing much of the damage. The insurer’s latest report puts the last three years of severe convective storm losses at $208 billion in today’s dollars, a number that should make property carriers pay attention.

What makes this story more than another weather warning is how fast the losses are spreading. Hail is hitting more places, smaller storms are creating bigger bills, and even low-severity events are stacking up into major annual losses for insurers.

Hail is now the main loss engine

Get the latest AI news in your inbox

Weekly picks of model releases, tools, and deep dives — no spam, unsubscribe anytime.

No spam. Unsubscribe at any time.

Allianz Commercial’s report says severe convective storms accounted for nearly half of all insured natural catastrophe losses globally last year. That alone would be enough to get underwriters’ attention, but the mix inside those losses matters even more: hail is responsible for as much as 50% to 80% of all severe convective storm losses, according to Allianz.

That is a major shift from the old mental model of hail as a nuisance peril. In the past, tornadoes, derechos, and other wind events often got the spotlight. Now hail is taking the biggest bite out of property books, especially where exposure has grown in suburbs, industrial corridors, and renewable energy sites.

The report also says severe convective storm losses in 2025 were 1.3 times the 10-year average, while U.S. insured losses were 1.4 times the average from 2015 to 2024. That is not a small drift. It is a sustained move upward that changes pricing, reinsurance buying, and claims staffing.

- $60 billion in global insured losses from severe convective storms in 2025

- $208 billion in losses over the last three years, adjusted to today’s dollars

- 50% to 80% of severe convective storm losses linked to hail

- 1.4x U.S. insured losses versus the 2015-2024 average

The storm risk is moving east

The geography matters as much as the totals. Allianz says drier conditions in the Great Plains have shifted Tornado Alley eastward into Southeastern states, where conditions favorable to tornadoes are showing up more often. That means more properties that were never priced like classic hail-and-wind territory are now getting hit more frequently.

The report also points to climate conditions that can produce stronger updrafts, which help form larger hailstones. Allianz says the most damaging hail is projected to increase by a broad range of 15% to 75% in frequency, depending on the climate scenario. That is a wide range, but even the low end is enough to alter loss expectations.

This is where the secondary damage starts to matter. Hail does not need to be grapefruit-sized to cause a serious claim. Small hail can clog roof drains, trap water on flat or low-slope roofs, and contribute to collapse. It can also create hidden damage that is easy to miss during a rushed inspection.

- Small hail can block drains and create ponding water on roofs

- Medium hail, about 0.2 to 1 inch, can damage crops, fruit, and glass

- Larger hail, about 1.2 to 2 inches, can break roofing materials and damage vehicles

- Extremely large hail, about 3 to 4 inches, can cause severe structural damage

What the people in the field are seeing

Andrew Higgins, technical manager for the Americas at Allianz Risk Consulting, said the rise in severe convective storm losses caught a lot of people off guard over the last five to 10 years. He said these losses used to sit below hurricane and typhoon losses, but now they are reaching the same range as other major perils.

“I would say that the losses that have resulted from severe convective storms have increased so much over the last five to 10 years, that it kind of caught a lot of people by surprise,” said Andrew Higgins, technical manager – Americas at Allianz Risk Consulting.

Higgins also pointed to a less obvious problem: smaller hailstones can still trigger expensive claims when they set off secondary damage. Roof drains clog, water pools, and roof structures fail. That is a claims pattern many building codes did not really plan for.

Don Giuliano, who works at weather technology firm Canopy Weather, said the Allianz findings match what he has been seeing for some time. He described severe convective storms as a primary risk, with hail often driving most of the losses as exposure grows in developed areas.

Giuliano also used a phrase that has been circulating in insurance circles: “kitty-cats.” He was referring to frequent, lower-severity events that look manageable one by one but add up to serious industry losses over a year. That matters because claims teams can underestimate the total cost of a storm season if they focus only on headline-grabbing disasters.

For claims organizations, the staffing issue is just as important as the weather. Geoffrey Conrad, a long-time claims professional who has trained adjusters, warned that the industry’s move away from field adjusters could increase missed damage, especially when hail is small and the damage is subtle.

Claims, roofs, and the hidden cost of small hail

The Allianz report says roofs and roof-mounted equipment are the most commonly damaged parts of a building in hail and high-wind events. That includes HVAC units and solar panels, which are now common on commercial buildings and can turn a weather event into a long-tail business interruption claim.

The biggest losses often come from water intrusion after a roof leak or from power outages that interrupt operations. In other words, the storm itself may last minutes, but the claim can run for weeks or months.

That is why the adjuster issue matters so much. If a newer desk adjuster misses collateral damage on a roof, siding, fence, or mailbox, the claim can be underpaid or reopened later. Conrad said hail damage is often broader than untrained eyes expect, and that problem gets worse as experienced field adjusters retire.

- Allianz says hail is the largest share of severe convective storm losses

- Munich Re has also noted rising hail-related severe convective storm frequency in Europe

- Swiss Re Institute said severe convective storms, floods, and wildfires drove 92% of global natural catastrophe insured losses in 2025

- Gallagher Re said severe convective storms drove at least 47% of insured losses in its January report

Those comparisons matter because they show Allianz is not alone. Swiss Re Institute estimated global natural catastrophe insured losses at $107 billion in 2025, with 92% tied to severe convective storms, floods, and wildfires. Gallagher Re said severe convective storms drove at least 47% of insured losses and totaled $208 billion over 2023, 2024, and 2025.

Put those numbers together and a pattern emerges: hail is no longer a side note in property insurance. It is a recurring, high-frequency loss driver that touches homes, warehouses, aircraft, manufacturing plants, and renewable power assets. If you price property in hail-prone regions, this is the risk you have to model first, not last.

What insurers should do next

The practical takeaway is simple: carriers need better hail exposure mapping, faster post-storm inspection workflows, and tighter attention to roof condition before renewals. If hail is now producing losses that rival named storms, then old assumptions about “secondary peril” pricing are too conservative.

The more interesting question is how quickly insurers will adapt their claims process to smaller hail events that create hidden damage. Will more carriers invest in better aerial imagery, sensor data, and specialized adjuster training, or will they keep finding out the hard way after the next heavy storm season?

My bet is that the next big underwriting fight will not be over whether hail is a major peril. That debate is over. The real fight is over how to price the repeat losses from smaller storms before they quietly eat into combined ratios again.

// Related Articles

- [IND]

Why AI infrastructure is now the real moat

- [IND]

Circle’s Agent Stack targets machine-speed payments

- [IND]

IREN signs Nvidia AI infrastructure pact

- [IND]

Circle launches Agent Stack for AI payments

- [IND]

Why Nebius’s AI Pivot Is More Real Than Hype

- [IND]

Nvidia backs Corning factories with billions