IMF Wants Caution as U.S. Opens Tokenization

The IMF urges controlled tokenization, even as U.S. regulators open permissionless rails for tokenized securities and bank capital treatment.

Tokenization is moving from theory to policy, and the split is getting harder to ignore. In March, U.S. banking regulators said tokenized securities on permissionless blockchains can be treated like conventional securities for capital purposes, while the IMF is warning that the same shift needs tight legal and technical guardrails.

That tension is the point of Tobias Adrian’s new IMF note, Tokenized Finance. Adrian, the IMF’s Financial Counsellor and head of its Monetary and Capital Markets Department, argues that tokenization changes where trust sits in the financial system, moving it away from institutions and toward shared infrastructure and code.

What the IMF is really worried about

Get the latest AI news in your inbox

Weekly picks of model releases, tools, and deep dives — no spam, unsubscribe anytime.

No spam. Unsubscribe at any time.

The IMF note does not treat tokenization as a simple database upgrade. Adrian frames it as a redesign of settlement, custody, and risk management, with programmable code replacing parts of the process that used to depend on intermediaries and manual controls.

That matters because the benefits are real. Tokenized assets can settle faster, reduce some credit exposures, and allow fractional ownership of instruments that were once hard to split up. But the IMF says those gains only hold if the system has public anchoring, clear legal rights, and a reliable way to resolve disputes when code and law collide.

The paper’s caution is also visible in what it emphasizes: permissioned systems, identifiable participants, override functions, and auditable smart contract logic. In other words, the IMF is comfortable with tokenization when someone can intervene if something breaks.

- Tokenization shifts trust from institutions to infrastructure and code.

- Fractionalization can widen access to assets that were previously illiquid or expensive.

- Smart contracts need legal certainty, or settlement risk gets pushed into a new layer.

- Emergency controls matter when financial code can move money faster than humans can react.

The U.S. is taking a different route

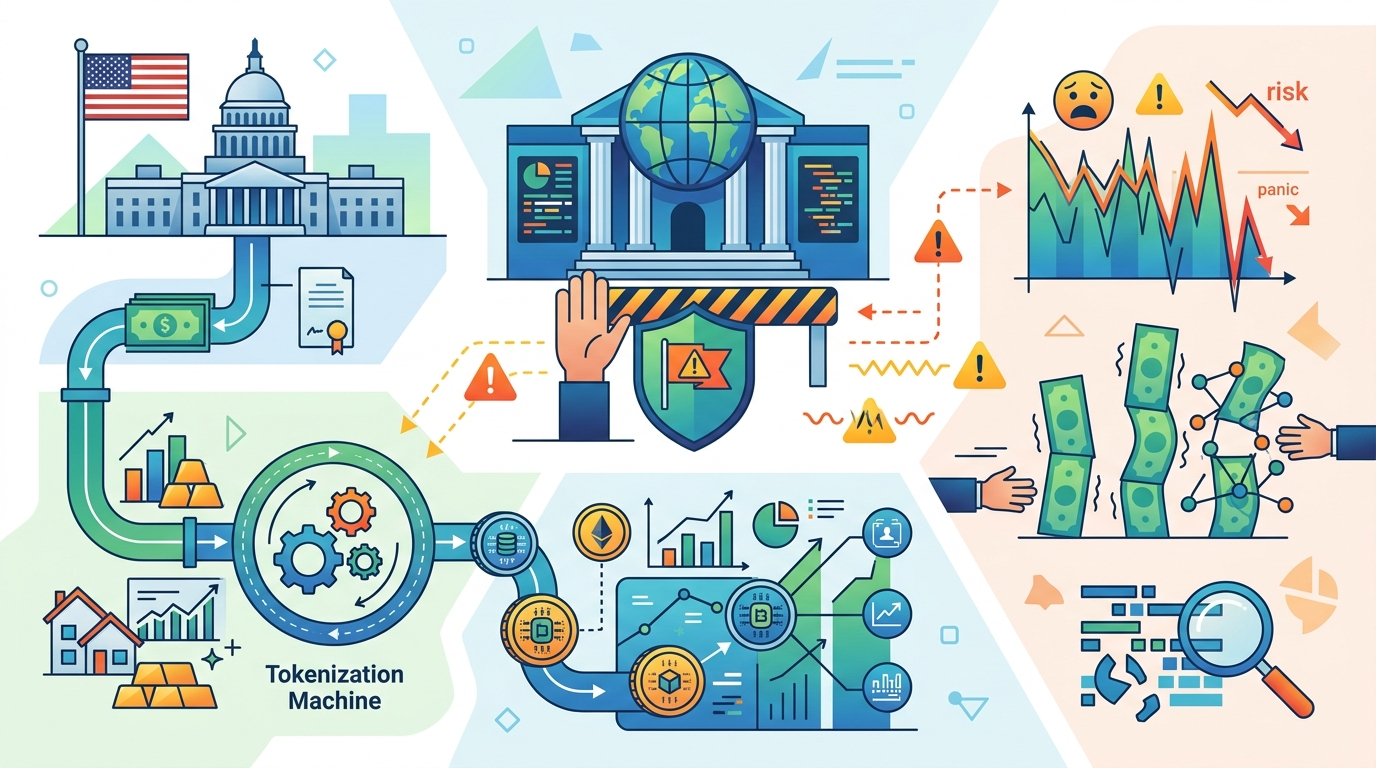

While the IMF is sketching a controlled model, U.S. regulators are becoming more open to permissionless infrastructure. In March, the Federal Reserve, OCC, and FDIC said banks can treat tokenized securities on permissionless blockchains the same way they treat conventional securities for capital purposes.

That is a meaningful shift because it lowers one of the biggest compliance barriers for financial institutions that want to test public chains. It does not mean every bank will rush in, but it does mean the default assumption is changing from “too risky to consider” to “review it like any other security exposure.”

The SEC has also issued a no-action letter to the DTC, allowing it to mint tokenized securities, including on permissionless infrastructure. That is a big deal because DTC sits near the center of U.S. market plumbing, and its approval signals that tokenized settlement is moving into mainstream market operations.

This is where the policy split becomes obvious. The IMF wants controlled environments with clear intervention points. The U.S. is testing whether public blockchains can fit inside existing financial rules without forcing everything into a private ledger.

Why permissionless chains worry global regulators

The Basel Committee is still reviewing its treatment of banks’ exposure to permissionless chains, and its current framework is far stricter than the U.S. approach. For now, assets on permissionless networks can attract a 1250% risk weight, which is so high that it effectively discourages bank balance sheet usage.

That number matters because it changes the economics. A bank can experiment with tokenized assets only if the capital charge does not make the activity uneconomic. Under the Basel treatment, public-chain exposure can become too expensive before the technology even proves itself.

The IMF’s caution fits that stance. Adrian is not rejecting tokenization; he is arguing that financial markets need a public backstop, legal clarity, and coordination across jurisdictions before tokenized systems can scale safely.

“The benefits of tokenization are potentially significant, but they can only be realized if the associated risks are properly managed.” — Tobias Adrian, IMF Financial Counsellor and head of the Monetary and Capital Markets Department

That quote captures the paper’s tone better than any policy summary could. The IMF is not trying to slow innovation for its own sake. It is saying that financial infrastructure is one place where speed without governance can turn efficiency gains into new failure modes.

What this means for banks, exchanges, and builders

For banks, the practical takeaway is that tokenization is no longer a fringe experiment. The U.S. is signaling that permissionless rails can be evaluated under existing rules, which opens the door for pilots that would have been hard to justify a year ago.

For exchanges and market infrastructure firms, the opportunity is bigger than tokenized assets alone. If settlement, custody, and transfer can move onto programmable rails, then post-trade workflows can shrink, reconciliation can get simpler, and certain asset classes can become easier to distribute.

For developers, the policy split creates a clear design choice. Build for permissionless networks and you get broader interoperability, stronger composability, and a larger ecosystem. Build for permissioned systems and you get more control, easier compliance, and clearer operational boundaries.

- Federal Reserve + OCC + FDIC: tokenized securities can be treated like conventional securities for capital purposes.

- SEC + DTC: tokenized securities can be minted under a no-action letter, including on public chains.

- Basel Committee: permissionless-chain exposure still faces a 1250% risk weight under current rules.

- IMF: tokenization needs legal certainty, public anchoring, and governance over smart contract logic.

If you want a useful mental model, think of this as a fight over where trust lives. The IMF wants trust anchored in institutions that can step in when needed. The U.S. is increasingly willing to see whether public infrastructure can carry that burden without collapsing under it.

Conclusion: the next test is policy, not code

The next phase of tokenization will not be decided by another whitepaper. It will be decided by whether regulators accept that public chains can support market plumbing without creating capital penalties, legal ambiguity, or settlement chaos.

My bet: the next 12 months will produce more pilot programs on permissionless infrastructure, but only a handful will touch core balance-sheet activity. The real question is simple: will global rulemakers update capital and custody rules fast enough to match the market’s pace, or will tokenization split into two worlds, one public and one tightly controlled?

// Related Articles

- [CHAIN]

UAE Web3 setup turns crypto rules into a checklist

- [CHAIN]

Five AI Futurist features shaping Futurist 2026

- [CHAIN]

Regulation Now Moves Bitcoin and Ethereum More Than War

- [CHAIN]

The SEC Crypto Rule Proposal Will Clean Up Crypto, Not Kill It

- [CHAIN]

Web3 platforms need fee discipline, not token theatrics, to make money

- [CHAIN]

Riyadh’s blockchain show proves Web3 is now infrastructure