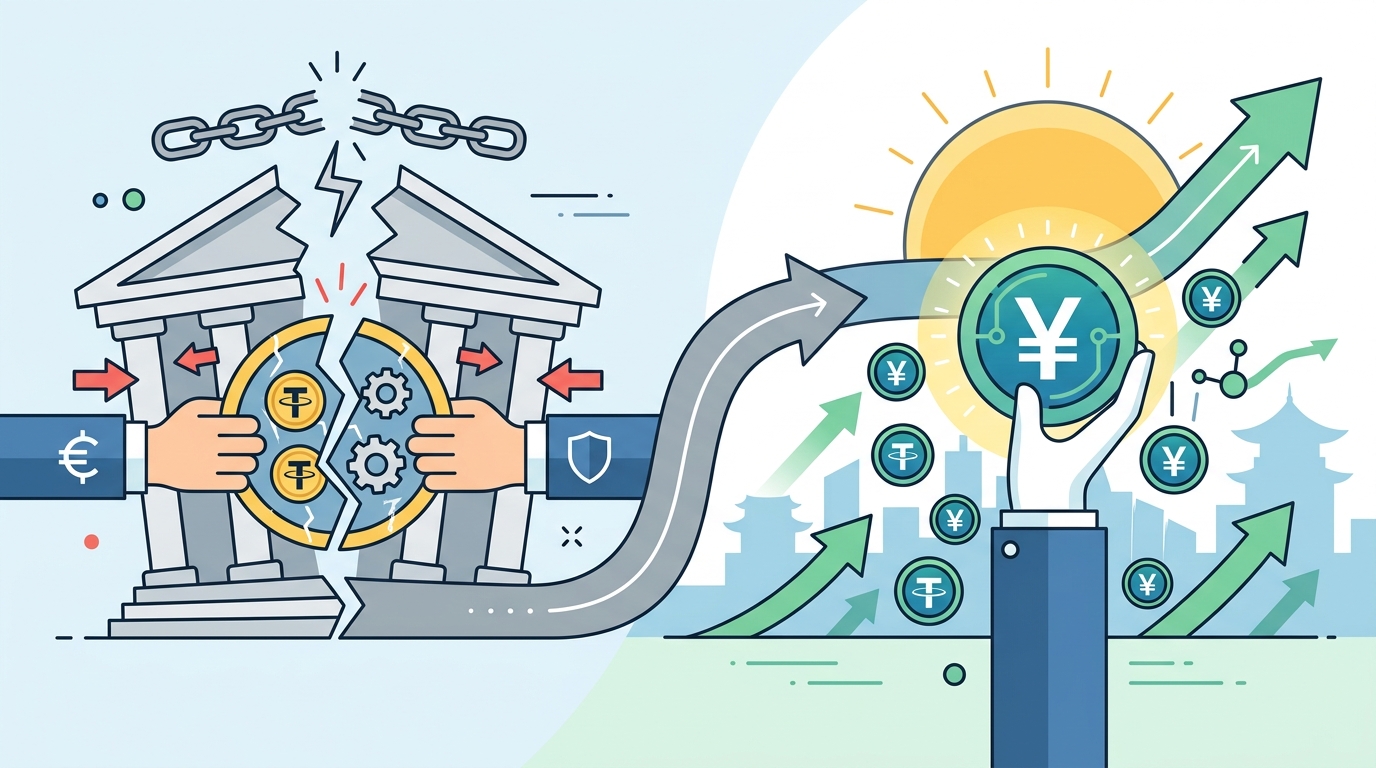

U.S. bank stablecoin fight could aid China

Banks want to block stablecoin interest. That could slow U.S. crypto adoption and give China more room to shape digital money.

More than $150 billion in stablecoins now circulate across crypto markets, and that number keeps climbing as dollars move on-chain faster than banks can settle transfers. The fight in Washington is about one narrow rule: whether Americans should earn interest on stablecoins held through digital platforms.

That sounds technical, but the policy choice matters a lot. If banks win and stablecoins become a dead-end payment tool instead of a yield-bearing cash alternative, the U.S. may protect old banking margins while giving foreign rivals more room to define how digital money works.

What stablecoins are really fighting over

Get the latest AI news in your inbox

Weekly picks of model releases, tools, and deep dives — no spam, unsubscribe anytime.

No spam. Unsubscribe at any time.

Stablecoins are tokens designed to track the dollar or another fiat currency. The big issuers, including Circle and Tether, back their tokens with cash, Treasury bills, and other short-term assets. That backing is why traders use them as a parking spot between trades, and why payment companies keep trying to make them useful outside crypto speculation.

The policy dispute in Congress is about whether stablecoin issuers, exchanges, and partner apps can pay interest or rewards on balances. Banks want that blocked. Crypto firms argue that if a stablecoin is a digital dollar, users should be able to earn something on it just like they can with a money market fund or a high-yield cash account.

That difference matters because stablecoins already function like a shadow payments rail. They settle in minutes, can move across borders without card networks, and cost far less than many traditional transfers. If U.S. rules make them less attractive, users will still look for yield elsewhere.

- Circle’s USDC is one of the most widely used regulated dollar tokens.

- Tether’s USDT has the largest market share in crypto trading pairs.

- Visa has already tested stablecoin settlement on public blockchains.

- PayPal launched PYUSD to bring digital dollars into mainstream payments.

Why banks are pushing back so hard

Banks are not worried about stablecoins as a concept. They are worried about deposit flight. If a customer can move cash into a token that pays interest through a wallet app, the bank loses a cheap source of funding. That pressure is especially sharp when rates are high and consumers are alert to better yields.

This is why big banking groups want a hard line between bank deposits and stablecoin balances. Their argument is simple: if digital dollars can earn interest, they start looking a lot like bank accounts without the same regulatory burden. The banks say that would distort competition and weaken the system that already backs consumer deposits.

The counterargument is just as simple. If Congress writes rules that make stablecoins less useful than they could be, the U.S. will slow private-sector payment innovation while other countries keep moving. That matters because financial infrastructure is one of the quiet ways power gets exported.

“The internet is becoming the town square for the global village of tomorrow.” — Vint Cerf

Cerf said that in 1999, and the line still fits this debate because payment rails are part of the internet’s plumbing. Whoever defines the rules for digital dollars helps define who gets paid, how fast, and at what cost.

China is watching the incentive structure

China has spent years building digital payment systems that reduce dependence on U.S.-controlled rails. Its central bank digital currency, the e-CNY, is still not a global reserve asset, but Beijing has already shown that it wants more control over cross-border money movement and more insulation from dollar-based systems.

If the U.S. turns stablecoins into a weaker product by banning interest and limiting their use, the result may not be that Americans return happily to bank deposits. A more likely outcome is that fintech firms look for workarounds, offshore platforms keep growing, and non-U.S. systems gain relative appeal in trade and settlement experiments.

That is the part policymakers often miss. The issue is not whether stablecoins replace banks. It is whether the U.S. wants to shape the next generation of digital dollar infrastructure or let others set the terms around it.

- China’s e-CNY has been tested in retail pilots across multiple cities.

- The Bank for International Settlements has pushed cross-border CBDC experiments through projects like mBridge.

- Stablecoin transfers can settle in minutes, while international bank wires often take longer and cost more.

- Dollar-backed tokens still dominate crypto liquidity, which gives the U.S. an opening if it writes sensible rules.

The comparison that matters most

Look at the incentives side by side. Banks want deposits protected, so they push for rules that keep interest inside the banking system. Crypto firms want stablecoins treated as programmable money, which means more flexibility, more competition, and more user choice.

Here is the practical difference if Congress sides with banks:

- Traditional banks keep low-cost deposits.

- Stablecoins remain useful for trading, but less attractive for everyday balances.

- Fintech apps lose a feature that could pull users away from legacy accounts.

- Foreign payment systems gain a talking point: the U.S. still treats digital cash like a threat, not infrastructure.

And if Congress sides with the crypto firms, banks will complain about deposit pressure, but users get a clearer path to earning yield on digital dollars. That would also make U.S.-backed stablecoins more competitive against offshore products that already move quickly and often operate with fewer constraints.

The best policy answer may be narrower than either camp wants. Congress could allow interest-like rewards while requiring clear reserve rules, consumer disclosures, and strict separation between insured deposits and token balances. That would preserve bank safety without making stablecoins pointless.

What happens next

The stablecoin fight is really a fight over who gets to define digital cash in the U.S. If lawmakers choose protection over competition, they may slow one part of crypto while pushing more activity offshore and giving China more room to promote its own rails.

My read is simple: the winning rule will shape payment behavior faster than most people expect. Watch whether Congress bans yield entirely or writes a middle path that lets stablecoins compete with bank products on price, speed, and utility. That decision will tell us whether the U.S. wants digital money to be an accessory to banking, or a product people actually use.

// Related Articles

- [CHAIN]

Crypto exchanges should show up in LATAM, not just advertise there

- [CHAIN]

UAE Web3 setup turns crypto rules into a checklist

- [CHAIN]

Five AI Futurist features shaping Futurist 2026

- [CHAIN]

Regulation Now Moves Bitcoin and Ethereum More Than War

- [CHAIN]

The SEC Crypto Rule Proposal Will Clean Up Crypto, Not Kill It

- [CHAIN]

Web3 platforms need fee discipline, not token theatrics, to make money